Can you really get guaranteed lifetime payments, even if you live to 100? Over

the past several years, many people have heard the income claims being touted

by fixed indexed annuities. But can these products really live up to 1hese

statements, especially given the longer life span of today’s retirees?

It’s true that people are living much longer now than ever before. Unfortunately, however, this longevity requires that savings be stretched to great lengths. That fact, coupled with the widespread disappearance of employer-provided pension plans, propels the biggest fear on the minds of most retirees today-running out of income before they run out of time.

There Is a Solution

Yet, there is a solution. Today, many investors are finding ways to turn their savings into a guaranteed

lifetime income stream in retirement-regardless of how long they live-and no matter what occurs in the market or even in the economy overall. And while it may sound too good to be true, it isn’t. They’re accomplishing this through the power of fixed indexed annuities.

A fixed indexed annuity essentially combines the security of a regular fixed annuity with the potential to earn additional interest that is linked to the return of an underlying market index, such as the S&P 500 or the Dow Jones Industrial Average. Yet, while the return is based on the performance of the market, your funds are not actually invested in it.

As with other types of annuities, the funds that are inside of a fixed indexed annuity are allowed to grow on a tax-deferred basis. This means that no tax will be due on the growth until 1he time of withdrawal.

However, unlike most other market-related investments, the fixed indexed annuity “resets” its value each

contract year, meaning that at the end of the contract year, the annuity’s ending value will become the next

year’s beginning value-thus essentially “locking in” the gain that was earned the prior year, never to be lost.

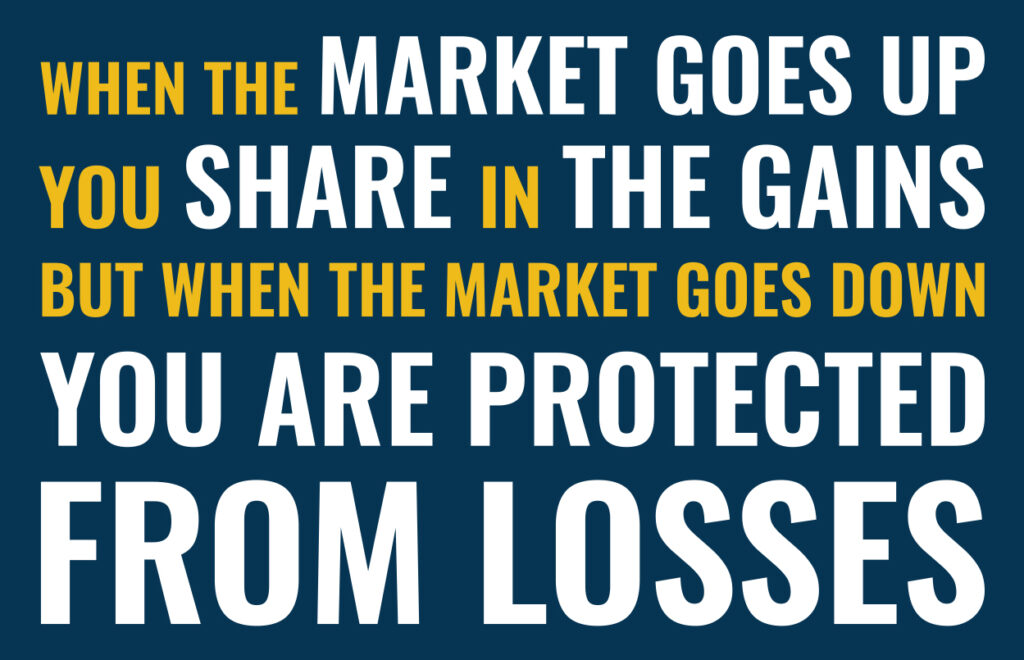

Because of this feature, you won’t lose principal in a fixed indexed annuity. So when the market goes up,

you share in the gains; but when the market goes down, you are protected from losses.

Creating Your Own “Self Pension”

In many ways, fixed indexed annuities have been likened to “self pension” plans. In fact, they do possess many similarities-starting with the fact that income can continue for1he remainder of the recipient’s life, no matter how long that is.

A joint income recipient can also be chosen. This way, a spouse or other individual can also be guaranteed

to receive income for the remainder of his or her lifetime, too. Moreover, if the income recipient passes away prior to receiving back all of the initial deposit, a named beneficiary can receive the difference in the form of a death benefit. This benefit is paid outside of probate, so your heirs won’t have to go through that costly and time-consuming process.

Taking the Next Step

Although fixed indexed annuities may not be ideal for everyone, they could be a wise choice if you are

seeking a guaranteed income in retirement but don’t want to worry about possible market losses with your

principal. These vehicles can also present a good option for those who want upward market potential,

without being subject to regular market volatility.

Unlike 401 (k)s and IRA plans, there are oftentimes no annual maximum contribution limits on the amount you can deposit into a fixed indexed annuity, which can really give your retirement savings a boost. With that in mind, a fixed indexed annuity could also be a good choice if you’ve already maxed out your retirement plan (or plans) and you are still seeking more options for tax-deferred growth.

So, while some people may think that it sounds “too good to be true,” the real truth is that yes, you can have guaranteed lifetime income payments from these fixed indexed annuities and basically create your own

pension.

By contacting us you may be provided with information about insurance products, including annuities, offered through Dave Mortach, Life & annuity licensed in Ohio.

*Mortach Financial offers a variety of products, a no fee promise is based off of the issuing company and may vary depending upon the product selected.

Fill out the form below to schedule your complimentary consultation and get a copy of Dave’s new book

*Make your check payable to Travis Mills Foundation and mail to: Mortach Financial, 3491 Napa Blvd Avon, OH 44011. One book per house hold. Terms and conditions may apply.