An unfortunate reality of life is ensuring you have a steady income stream after one spouse passes away. In many cases, a surviving spouse can end up losing a significant portion of his or her income stream. For many individuals, retirement only lasts a short period of time following the death of a husband or wife.

For example, pensions are designed to stop completely or to be drastically reduced upon the

death of the primary recipient. Social Security income can also be reduced upon the passing of

your spouse. These reductions in retirement income can result in an abrupt change in lifestyle.

Ask yourself this question: With the current structure of your retirement plan would you or your

spouse be able to maintain an adequate lifestyle if one of you were to die? If not, you must

consider what could happen to your retirement lifestyle.

Regardless of how your pension has been designed or whether you have a pension plan at all, there are ways that you can ensure that both spouses are able to maintain an ongoing income

stream throughout your lives. A fixed indexed annuity helps to provide spouses with a stable

retirement income.

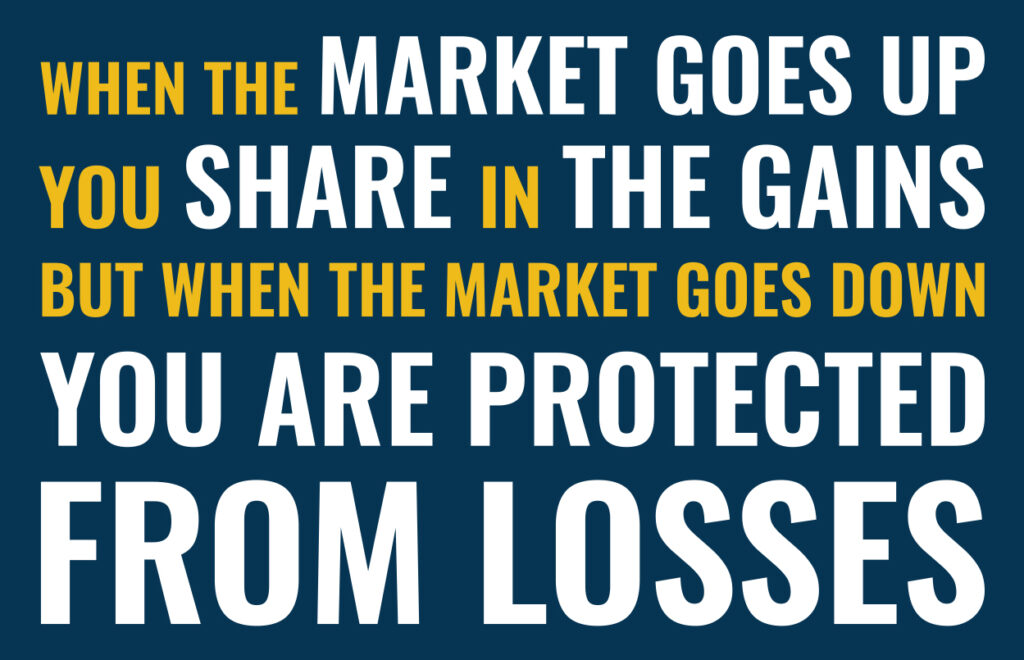

Throughout your working years, a fixed indexed annuity will allow you to take advantage of growth opportunities in the market. Additionally, in down market years, these types of annuities do not subject you to downside market risk. These investments provide you with safety of

principal.

Just like other types of annuities, the funds are allowed to grow on a tax-defered basis. No truces

are due on the growth of your funds until the time they are withdrawn. This can allow your fixed indexed annuity money to compound exponentially over time.

This can provide you with the assurance that upon the first spouse’s death, even if other income payments are lost or reduced, income from the fixed indexed annuity will continue.

While losing your spouse can be extremely difficult, this loss doesn’t have to include loss of retirement income or a possible drastic reduction in lifestyle. By planning ahead using a fixed indexed annuity, both spouses can have a set ongoing lifetime income – regardless of how long that may be