So, what exactly is most people’s idea of a stress-free retirement? In many cases, it begins with having a steady, ongoing stream of reliable income-income that can be counted on to pay living expenses, month in and month out, and income that won’t be depleted, regardless of how long you live.

However, getting there can be a challenge. There are all sorts of obstacles along the way, such as potential

market volatility and inflation. But what if there was a strategy that could allow retirement funds the growth of the

market, along with the safety of the bank? There is!

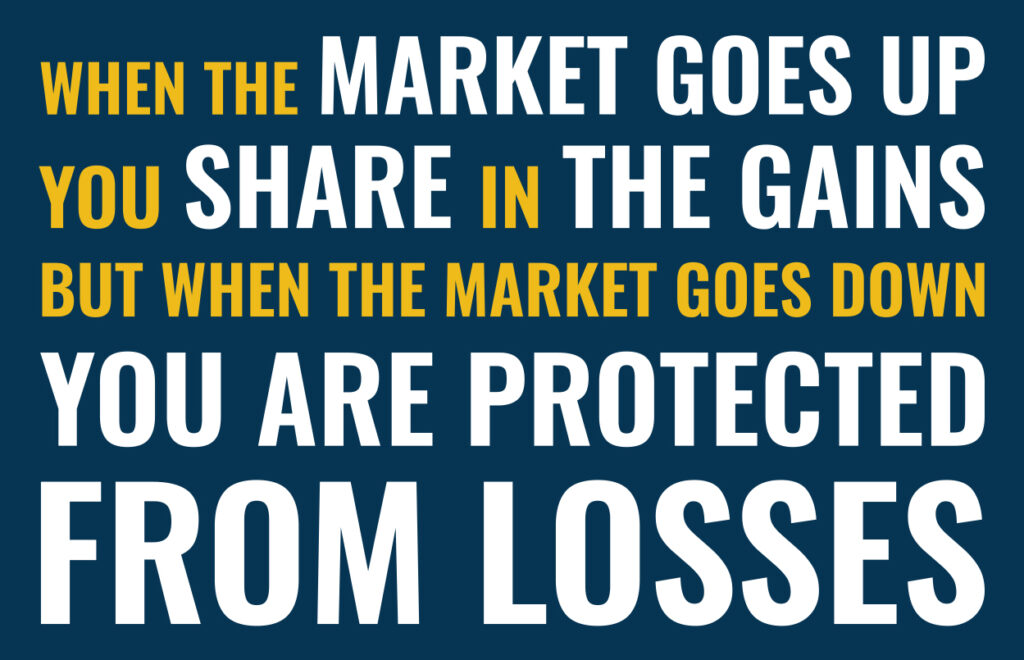

Fixed indexed annuities provide the ability to grow funds based on the performance of an underlying market index,

such as the S&P 500 or the Dow Jones Industrial Average. Yet, while your annuity funds track the index, they

aren’t actually invested in the market.

Just like other annuities, your funds are allowed to grow on a tax-deferred basis. This means that no tax is due on the gain until the time they’re withdrawn. Over time, this can allow funds to compound exponentially.

What about market down years? Here’s where fixed indexed annuities really shine. If the index has a negative year, your annuity is credited with zero-meaning that, even though you have no gain for the year, you also have no

losses. This protects principal in down market years-a nice feature for years like 2008!

When it’s time to convert the annuity to income, fixed indexed annuities offer a lifetime income option-meaning

that you will receive ongoing income for life, no matter how long you may live. By choosing the joint life option, you

and your spouse (or you and another named individual) will each receive guaranteed lifetime income.

In addition to providing growth, principal protection, and guaranteed lifetime income, fixed indexed annuities can

provide additional benefits as well. For example, if the income recipient passes away without receiving back all of

their initial deposit, the difference will be paid out to a named beneficiary, and these funds will avoid the costly and

time consuming process of probate. In addition, in many states, annuity funds are also protected from creditors.

While many people may be lamenting the disappearance of the defined benefit pension plan, the fixed indexed annuity has essentially brought it back into the hands of consumers, but this time, you control it.

Although all of this may sound too good to be true, it really isn’t. But insurance companies are the only entities that

can truly offer this type of product. Why? Because insurance companies are the only companies that are on “both

sides on the fence” in certain types of financial transactions.

Here’s how it works. When a person buys a life insurance policy, the risk to the insurance company is that the individual will “die too soon.” Alternatively, when a person buys an annuity, the insurance company is risking that the individual will live a long time.

Today, because people are living so much longer, insurance companies aren’t having to pay out as many large death benefit claims, so they are in turn able to offer these lifetime income products like no other type of financial company can-not banks, not brokerage houses, and not mutual fund companies.

Setting Up Your Income Solution

Even when some things sound too far-fetched, a simple explanation can bring them into much clearer focus. For

those who are seeking to grow and protect principal on a tax-deferred basis, as well as to convert those funds into an ongoing guaranteed lifetime income in retirement-regardless of market condition-the good news is that you now have

a way to create your own personal pension. The only question is when do you want to start?