How Retirement Planning Has Changed

Today, the face of retirement planning has changed a great deal, starting with who takes responsibility for living expenses, as well as ensuring that received income will continue throughout a retiree’s life.

While defined benefit pension plans provide a number of benefits to participants, most employers have been moving away from these types of plans. One reason for this is the substantial expense. Defined benefit plans require employee contributions regardless of profit earnings. This can make a defined benefit plan a liability for a business that offers it.

Due to increased global competition and other financial obligations, pensions often don’t make sense to offer from a company standpoint. With that in mind, many companies have started providing “defined contribution” plans such as the 401(k). According to the Bureau of Labor Statistics, last year only 25% of workers in the U.S. had access to defined benefit plans—most of which are geared towards large companies with 500 or more employees and government workers.1

A defined contribution plan is one where the contribution is set, or “defined.” In 2015, the maximum amount may contribute into a 401(k) plan is $18,000 (age 49 and under). Those 50 or over are allowed to contribute an additional $6,000 per year.

Private Sector Workers Participating in Employment-Based Retirement Plans

Unlike the defined benefit pension plan, a defined contribution plan leaves everything up to the employee. In addition, the contributions all come from the employee unless the employer makes a matching contribution, which is based on the percentage that the employee deposits into the plan.defined benefit plan a liability for a business that offers it.

Employees involved in a defined contribution plan are also responsible for choosing how their funds will be invested. In most instances, the sponsoring employer offers a variety of investment choices. In some cases, the employer’s own shares of stock may also be an option. Funds inside of a defined contribution plan are allowed to grow on a tax-deferred basis, but cannot be withdrawn without a 10% early withdrawal penalty.

How to Create Your Own Personal Pension Plan

With the disappearance of corporate pension plans, you can create a personalized pension plan that gives you control over your retirement income and principal.

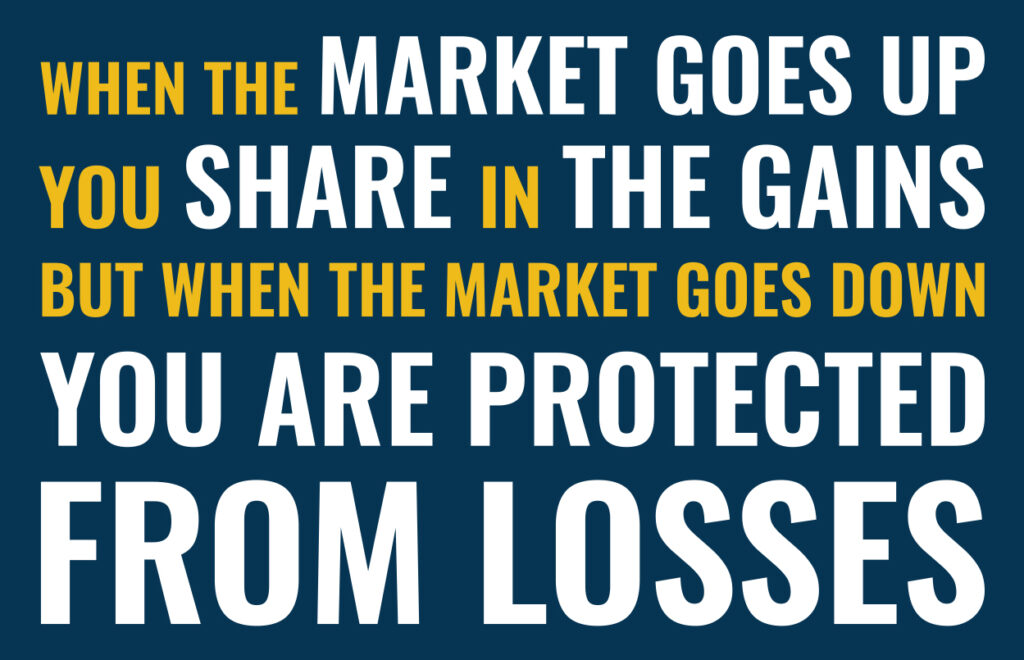

A fixed indexed annuity (FIA) offers a combination of benefits, including the opportunity for market-linked growth at credited interest rate, protection of principal, and a guaranteed stream of income for the remainder of your life. A FIA can do this because of the protection and guarantees supported by the insurer’s claims-paying ability and financial strength of the insurer.

Similar to other types of annuities, a fixed indexed annuity grows on a tax-deferred basis, allowing the money to compound over time. Many of these vehicles also offer a death benefit as well to help recoup invested funds should the annuity holder pass away.

Fixed indexed annuities also provide a way to keep up with inflation, which is a vital feature given today’s longer life expectancies and price inflation.

Additionally, most FIAs offer optional guarantees. For instance, by increasing the annuity holder’s guaranteed lifetime income payment each year, there is a positive interest credit to the account value.

Even though pension plans are disappearing, you can still control your retirement income. With a fixed indexed annuity, you can control, protect, and potentially grow your income.