Thankfully, there is an income strategy for retirement planning that does not require you to risk your principal or lose out to inflation. This strategy is fixed indexed annuities. With annuities, your principal is guaranteed by the insurers’ claims-paying ability and financial strength of the issuing insurance company.

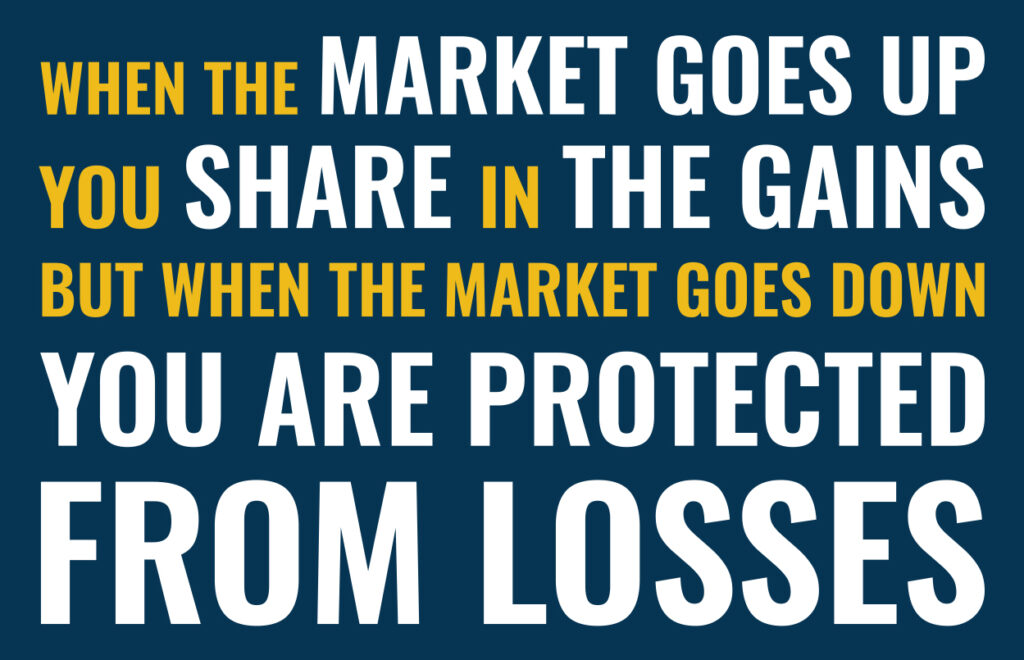

When considering your options for retirement income, there is a better way to position your savings so that you can generate an ongoing income. You can accomplish this regardless of what happens in the market, and reduce the fear of running out of money, through a fixed indexed annuity. As with other types of annuities, a fixed indexed annuity, or FIA, allows your funds to grow tax-deferred. This means the gain remains tax-free until the time of withdrawal. However, these annuities differ from a regular fixed annuity because funds can grow based upon the upward movement of an underlying index, such as the S&P 500 or Dow Jones.

One of the key benefits of an FIA is that if the underlying index has a negative performing time frame, the annuity owner is still guaranteed a minimum amount of return each year. In other words, your principal won’t be subject to the downward movements of the market because of a contractual guarantee provided by the insurers’ claims-paying ability and financial strength of the issuing insurance company.

When the time comes to convert to an income stream, a fixed indexed annuity can also provide you with a number of key advantages. First, the lifetime income option allows you to receive income payments for the remainder of your life. FIAs also can be issued with various types of income riders that can supply lifetime income payments to the policyholder, even if the annuity has not been converted to income. This can leave you in control of the remainder balance of the account. Such riders are calculated separately from the rest of the annuity, and these riders will typically offer a specific accumulation rate for a certain number of years.

Once the lifetime income payments begin, the value of the income pool is used to determine the amount of income that will be paid out. The income riders that allow for lifetime income are often used as a way to allow policyholders to supplement retirement income, without the worry of outliving your funds. These riders continue to pay out even if the FIA account value is zero.

With a fixed indexed annuity, you can rely on a steady stream of income – regardless of what occurs in the market or the economy. If you choose the joint life option, you and the joint annuitant can each receive income for the remainder of both your lives.