We’re Sorry, You’ve Reached a Number That Is No Longer in Service

Certainly, saving money is an essential step in the process of having a fruitful retirement.

For most of our adult lives, we’re taught that setting aside at least 10 percent of our

income is a suggested benchmark to hitting our future goals. And, as baby boomers reach their mid-60s, we’ve seen more financial services commercials touting how you need to reach your ideal savings “number” before you can retire.

Unfortunately, these ads focus solely on the accumulation of funds during the time that you are still working and saving money, with little to no talk at all about what you should do once you’ve left the world of employment.

But the truth is, when you get to retirement, you aren’t going to live on net worth — you’re going to need to live on income. It’s income that will pay the mortgage, income that will pay the electric bill, and income that will pay for groceries. So, the question is, how do you take what you’ve saved and convert those dollars into an ongoing income that will last throughout the remainder of your life?

The Lifetime Income Solution

While most of us know how to save, few are deeply familiar with how to convert those dollars into a lifetime

income. Contrary to the famous television commercials, there is no “magic number” when you reach retirement.

On the day your employment stops, everything changes. You will need to have a way of making the distributions from your savings — ideally coupled with the option for income from Social Security and possibly a pension — last for the remainder of your life.

The good news is, there is a solution. By including fixed indexed annuities into the mix, many investors are not only able to provide themselves with lifetime income in retirement but also a way to protect income during their accumulation years while allowing growth potential.

In many ways, a fixed indexed annuity can be said to offer the “best of both worlds.” This is because it provides growth potential and principal protection during the accumulation phase, and the option for ongoing lifetime income after that.

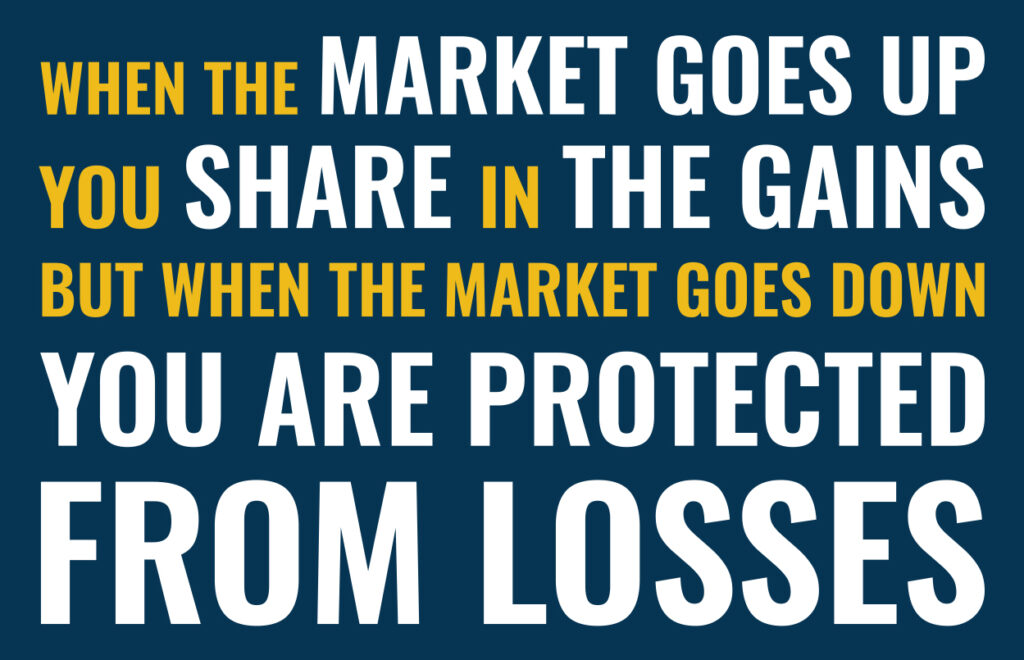

What makes these annuities different from regular fixed annuities is that the growth inside the account is based on the performance of an underlying index, and the value of the index is tied to a stock market or other type of index. Some of the more common indices that are tracked are the S&P 500 or the MIA. Yet, although the annuity tracks the index, funds are not actually invested in the market.

In “up” market years, the annuity will be credited with a positive return. However, in “down” market years, the annuity is credited with zero. Therefore, fixed indexed annuity holders do not lose principal. In addition, the annuity’s value is “reset” each contract year, locking in the prior year’s gains — never to be lost in future years — regardless of what happens in the market. This can provide you with solid growth over time.

During the income phase, the fixed indexed annuity offers the option to increase its income payments in order to help keep pace with inflation. This can help to protect your purchasing power throughout the years.

If you should pass away prior to receiving back all of your initial deposit in the form of annuity income, your named beneficiary will receive the difference in the form of a death benefit. These funds will avoid the costly and time-consuming probate process.

Is This a Solution For You?

For those who have a goal of creating a guaranteed source of lifetime income, along with building and protecting principal, a fixed indexed annuity can meet all of these needs combined, while at the same time offering tax advantages and reducing a great deal of uncertainty going forward.

Don’t be confused by trying to reach your ideal “number.” We’ve been taught wrong in the past about what’s really important to focus on, in order to have a successful retirement. But ongoing lifetime retirement income — now that’s peace of mind!