In the past, setting up a retirement withdrawal strategy involved taking a small percentage from a retiree’s overall portfolio and letting the remaining capital continue to grow. These withdrawals, coupled with Social Security benefits and employer-sponsored pensions, were normally enough for individuals to live comfortably for the remainder of their golden years.

Today, things have changed. Because most companies no longer offer defined benefit pension plans, individuals must ensure that they have enough income for their retirement. Luckily, there is a way to manage your retirement income by investing in a fixed indexed annuity.

With a fixed indexed annuity, or FIA, income payments can be set up so that they will last for the remainder of your life. The income payment can be received on an annual, quarterly, or monthly basis. Having this type of control allows you to know exactly how much you have coming in, and how much can be allocated for living expenses.

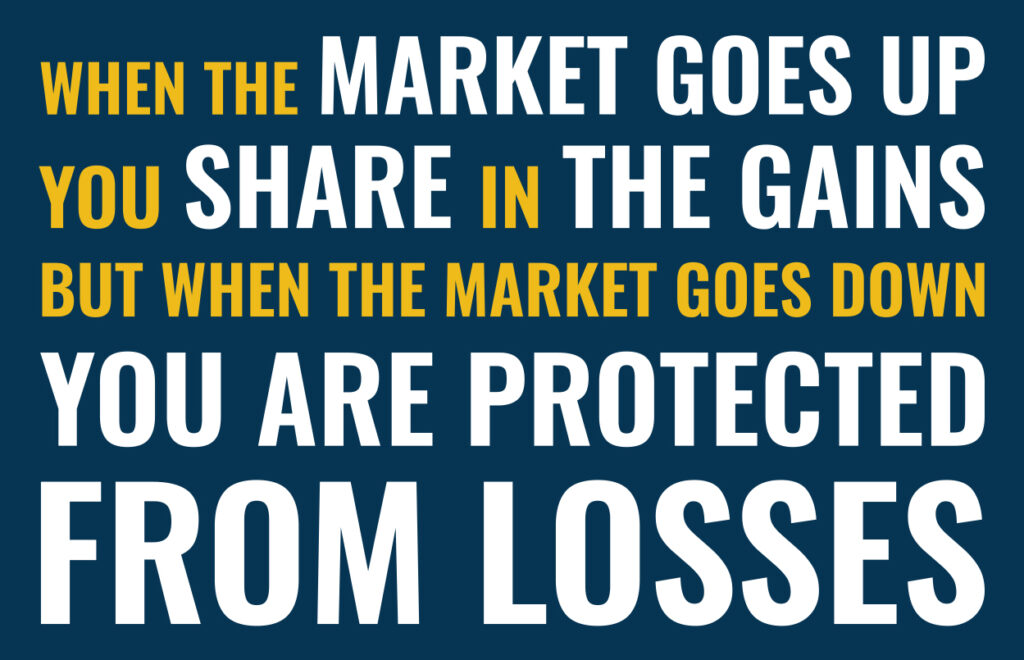

In addition to income benefits, a fixed indexed annuity can offer an array of other advantages. For instance, during the accumulation phase these annuities provide their owners with the ability to take part in the growth of the underlying index. However, in down markets, investors are not subject to negative market performance. This occurs because contractual guarantees are based upon the insurer’s claims-paying ability and financial strength of the issuing insurance company.

By taking control of your retirement income with a fixed indexed annuity, you will know how much income to expect and when you will receive it. You are also on track to solve the problem of outliving your assets. In doing so, you have less to worry about and more time to enjoy your retirement.